Estrategia - Relaciones Internacionales - Historia y Cultura de la Guerra - Hardware militar.

Nuestro lema: "Conocer para obrar" Nuestra finalidad es promover el conocimiento y el debate de temas vinculados con el arte y la ciencia militar. La elección de los artículos busca reflejar todas las opiniones. Al margen de su atribución ideológica. A los efectos de promover el pensamiento crítico de los lectores.

Our career choices are often shaped by our personal tragedies. Someone who loses a parent to cancer may decide to become an oncologist. Someone who grows up around crime may go into criminal psychology. I think about this principle when I see Argentinian macroeconomists.

If you go to macroeconomics conferences and read macroeconomics papers, you quickly see that Argentinians are hugely overrepresented in the field. For example, take Ivan Werning, one of the rising superstars in the macro field. Narayana Kocherlakota, president of the Minneapolis Fed, credits a paper by Werning as the thing that changed his mind about keeping interest rates low. Kocherlakota himself is no academic slouch, so it speaks volumes that he would alter his entire outlook based on Werning’s insights.

Another Argentinian superstar is Columbia’s Guillermo Calvo. Calvo is responsible for one of the key mathematical techniques that powers New Keynesian economic models, which are now the dominant type used in business-cycle theory. A couple other prominent examples are Massachusetts Institute of Technology’s Ricardo Caballero and Alberto Cavallo. The list goes on and on; I could fill two full-length Bloomberg View articles singing the praises of star macroeconomists from Argentina, and still leave some off the list.

But if Argentinians are stars in the halls of American academia, they are veritable celebrities in their home countries. Back in 2014, the Economist ran a story about macroeconomists in Argentina dating star actresses and boasting hundreds of thousands of Twitter followers. It’s enough to make me think I picked the wrong profession!

So here’s the question: Why has there been such a flood of Argentinian talent into macroeconomics? Here’s where the idea of personal tragedy comes in. Argentina is a classic example of a macroeconomic basket case. It’s quite possibly the only country where bad macroeconomic policy sent a country into long-term decline.

The past century has been an unmitigated failure for Argentina’s economy. A century ago, the country was firmly in the ranks of the developed nations, boasting a per capita gross domestic product about three-quarters that of the U.S. (about where Japan and the U.K. stand today). Since then, the figure has declined relentlessly, as Argentina stagnated and the rest of the world pulled ahead. As of today, Argentina is down to about a third of U.S. income levels, putting it solidly in the ranks of middle-income countries.

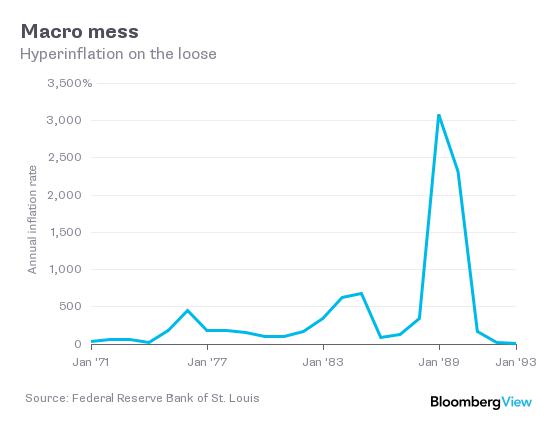

That sorry record has been riddled with macroeconomic disasters. Here is a picture of the Argentinian rate of inflation:

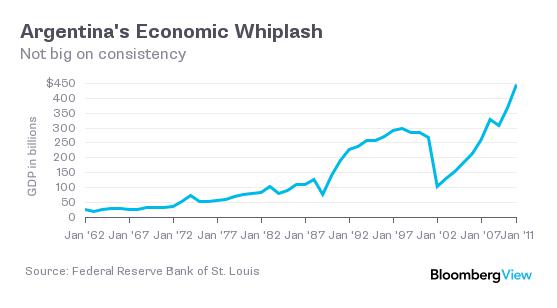

As you can see, Argentina had hyperinflations three times in the late 20th century. As for GDP growth, where most countries have smooth upward trends punctuated by minor stumbles, Argentina has a sawtooth pattern of booms and catastrophes:

Note how in the early 2000s, GDP -- not GDP growth, but actual income per person -- plunged by about two-thirds. That is a disaster on a level usually seen only by the likes of Russia or Zimbabwe.

That GDP plunge came from a sovereign debt default -- a hallowed Argentinian tradition. The country experienced its first sovereign default just 11 years after achieving independence in 1816, and it didn’t stop there. Argentina defaulted in 1890, and some of its provinces defaulted in both 1915 and 1930. It narrowly avoided default in 1956, then defaulted on its external debt in 1982 and its internal debt in 1989. Then came the big one, in 2001. Argentina’s epic default was the worst in history at the time.

As you might expect, this macroeconomic turmoil has been accompanied by political turmoil. Sometimes political instability is the cause of macroeconomic instability, and sometimes the reverse is true. Argentina’s history is a sorry litany of coups, dictatorships, unstable democracies, massive economic interventions, riots and unrest.

No wonder Argentina’s best and brightest go into macroeconomics. What else are they going to do with their smarts? If they go into engineering, the chances are high that bad macroeconomic policy-making will simply force their companies into bankruptcy. In macro, at least they might have a shot at finding a fix for their country’s apparent curse.

The sad thing is that they almost certainly don’t have a shot. Economists are not very good at understanding the vagaries of politics, mass movements, power transitions and the like. Nor is anyone else, for that matter. Studying optimal monetary policy or fiscal policy is well and good, but it’s a lot more likely to help a stable country like the U.S. than an unstable country like Argentina. The best macroeconomic policies are no good if they depend on the worst people to implement them.

So while the torrent of talent from Argentina has enriched the macroeconomics profession, it won’t be able to heal Argentina’s troubles. For that, Argentina needs stable, inclusive institutions -- civil society, a stable democracy, a state that tries to encourage economic development instead of lurching from crisis to crisis. That is something that, for now, no theory can tell us how to create.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

No hay comentarios:

Publicar un comentario